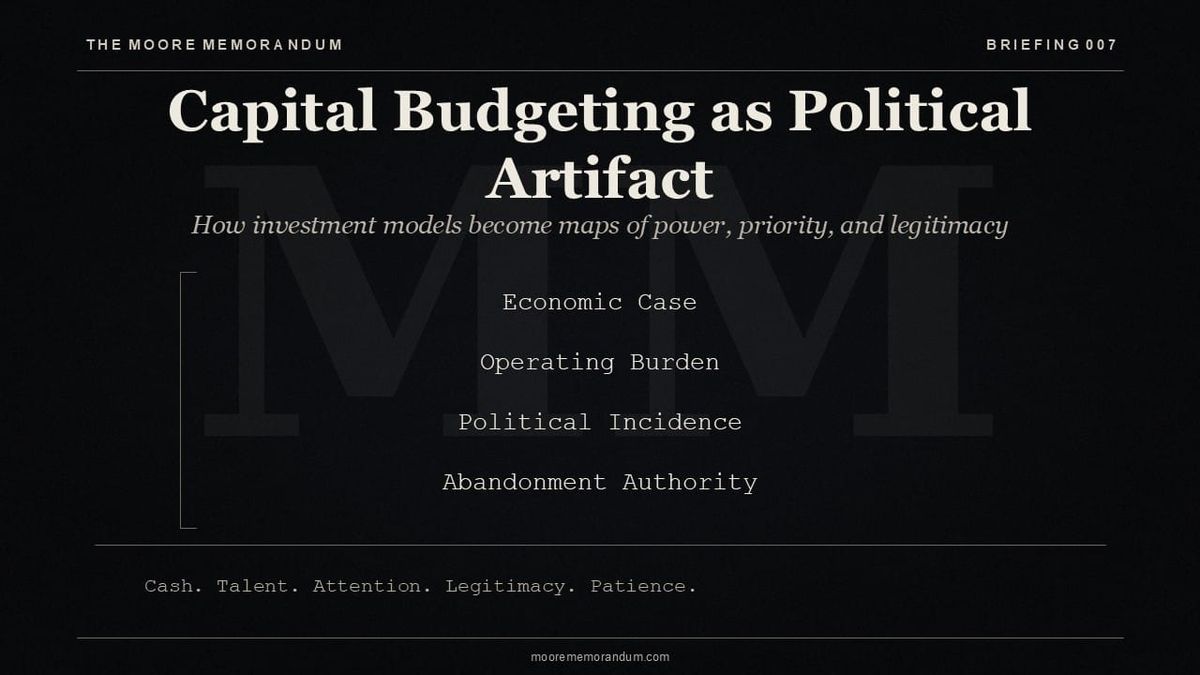

The Moore Memorandum — Briefing #007

Capital budgeting decides which future receives cash, talent, attention, legitimacy, and patience. Briefing 007 examines how investment models become maps of economic claim, operating burden, political incidence, and abandonment authority.

Capital Budgeting as Political Artifact

How investment models become internal maps of power, priority, and legitimacy

Executive Summary

Capital budgeting is the formal language through which an organization allocates scarce commitment: cash, talent, executive attention, operating tolerance, and future strategic freedom.

The model records the economic case. The approval process reveals the institutional case: who sponsors the project, whose priorities receive protection, which functions carry the burden, and which future the firm is prepared to legitimate.

A capital request becomes political when the model is built to ratify a preferred course of action rather than discipline it. The warning signs are familiar: accommodating discount rates, selective comparables, underpriced implementation burden, strategic labels without measurement, and renewed funding after weak interim evidence.

Sound governance treats capital budgeting as decision architecture. Major proposals should disclose the economic claim, strategic claim, operating burden, political incidence, stage-gates, and abandonment authority.

The mature board asks a stronger question than whether the project clears the hurdle rate:

Whose future does this model protect, and what evidence would require withdrawal?

1. The Pattern

Capital budgeting arrives in the language of finance: NPV, IRR, payback period, hurdle rate, sensitivity analysis, terminal value, scenario range.

That language is necessary. It gives the proposal a common grammar and permits comparison across competing uses of capital.

The actual decision frequently turns on a broader institutional field:

- which executive sponsors the proposal;

- which division needs growth credit;

- which capability the company wants to be seen as possessing;

- which legacy asset requires continued justification;

- which function carries the integration work;

- which cost sits inside the model and which cost migrates to operations;

- which alternative lacks a powerful advocate;

- which future receives patience.

The model is therefore a political artifact in the proper sense of the word. It records an allocation of power, priority, and legitimacy. Bower’s resource-allocation tradition is useful here because it treats strategy formation and corporate investment as embedded organizational processes rather than detached calculations; later resource-allocation work likewise treats everyday managerial decisions as central to how strategy forms inside firms.

The governing question:

What must be true economically, operationally, and institutionally for this proposal to deserve commitment?

2. The Political Work of the Model

A capital model performs four kinds of internal work.

1. It legitimates a preferred future

A project with a model becomes administratively real. It can enter the budget cycle, recruit allies, request diligence, command meeting time, and acquire a place in the company’s future.

The existence of a model does not prove the case. It gives the case standing.

2. It translates ambition into acceptable language

Executives rarely present capital requests in terms of divisional status, personal legacy, or internal positioning. They present growth, margin expansion, synergies, option value, cost reduction, resilience, or strategic control.

That translation can be legitimate. It becomes suspect when the financial vocabulary conceals the real institutional motive.

3. It transfers burden

A proposal may look attractive because the sponsor captures the upside narrative while other functions absorb the work.

The implementation burden may sit with operations.

The integration burden may sit with IT.

The customer burden may sit with support.

The training burden may sit with field teams.

The control burden may sit with legal, finance, or compliance.

The opportunity cost may sit nowhere.

The sponsor owns the presentation. The enterprise owns the consequence.

4. It creates a record of acceptable belief

Once approved, the model becomes part of the organization’s memory. The company can later continue funding the project because the earlier approval made the project legitimate.

This is where escalation of commitment enters. Staw’s 1976 work on escalating commitment is the canonical starting point: decision-makers may continue investing in a chosen course after adverse evidence, especially when prior resources and responsibility are already attached.

3. Where Formal Rationality Becomes Thin

The formal chain is clean:

Project → Forecast → Valuation → Decision

The organizational chain is often closer to this:

Sponsor → Narrative → Model → Coalition → Approval → Interpretation

The second chain explains why technically sound finance can coexist with poor capital discipline.

The behavioral theory of the firm is helpful because it treats the firm as a coalition with multiple goals, bounded rationality, aspiration levels, organizational slack, negotiated priorities, and satisficing behavior. Cyert and March’s work replaced the image of a single maximizing actor with a more realistic account of organizations as coalitions that search, bargain, and settle for acceptable outcomes under imperfect information.

In capital budgeting, the proposal is rarely evaluated by “the firm” in the abstract. It is evaluated by functions with different obligations:

| Function | Usual Interest |

|---|---|

| Finance | discipline, comparability, capital efficiency |

| Strategy | coherence, positioning, long-term option value |

| Operations | feasibility, absorption capacity, execution risk |

| Product | roadmap control and customer value |

| Sales | market coverage and revenue narrative |

| IT / Systems | integration, security, architecture |

| Legal / Compliance | authority, obligations, regulatory exposure |

| Sponsor | approval, resources, internal standing |

| Board | process quality, risk, stewardship |

The political artifact emerges when these different interests are compressed into one NPV.

4. Seven Failure Modes

Failure Mode 1 — Sponsor Premium

Some proposals receive credibility because of the person presenting them.

The project borrows the sponsor’s status: prior success, proximity to the CEO, control of a strategic narrative, or reputation for execution. The same evidence may receive different treatment when presented by a less powerful owner.

Governance test: Review the proposal without sponsor identity. Ask whether the evidence still supports the same capital release.

Failure Mode 2 — Strategic Exception

The project misses ordinary investment thresholds and is then advanced through the language of strategy.

Strategic projects can warrant different treatment. Capabilities, options, resilience, defensive positioning, and long-horizon control may deserve capital even when near-term returns are uncertain. The abuse occurs when “strategic” becomes a substitute for measurement.

Governance test: Require the proposal to name the strategic asset, the measurement proxy, the stage-gate, and the abandonment condition.

Failure Mode 3 — Hidden Operating Burden

The model captures capital expenditure and direct operating expense while omitting the system load:

| Burden | Typical Location |

|---|---|

| implementation | operations |

| integration | IT / data / security |

| training | field teams |

| customer disruption | support / success |

| quality risk | operations / compliance |

| management attention | senior leadership |

| change management | middle management |

| governance | legal / finance / board committees |

The project looks profitable because the burden has been allocated outside the spreadsheet.

Governance test: Require an operating-absorption review signed by the functions that will carry the work.

Failure Mode 4 — Selective Scenario Discipline

Downside scenarios appear in the appendix and vanish from the decision.

The base case becomes the political case. The upside case becomes the sponsor’s voice. The downside case becomes a formal gesture.

Governance test: Every downside scenario should produce a decision: reduce scope, delay hiring, stage capital, renegotiate terms, partner, or decline.

Failure Mode 5 — Incentive Inversion

The organization rewards project approval more visibly than value delivered.

Sponsor status rises when a project is funded. Budgets expand. Teams grow. Strategic visibility increases. The organization then hopes the sponsor will maintain discipline after receiving the reward.

Kerr’s classic warning on “rewarding A while hoping for B” remains useful: organizations often design incentives that reward one behavior while claiming to desire another.

Governance test: Track sponsor credibility against post-approval outcomes, not approval volume.

Failure Mode 6 — Convergent Ambiguity

Problems, solutions, sponsors, and meetings sometimes converge because the organization has a decision window open.

Cohen, March, and Olsen’s garbage can model describes decision settings with problematic preferences, unclear technology, and fluid participation. In such settings, problems, solutions, participants, and choice opportunities may come together in unstable ways.

Capital budgeting often has these qualities: ambiguous goals, incomplete causal knowledge, shifting participants, and proposals seeking a moment of approval.

Governance test: Require the proposal to state the problem, rejected alternatives, timing rationale, and reason this is the right moment for commitment.

Failure Mode 7 — Escalation After Weak Evidence

The project underperforms. Management requests more capital to finish the work, reach scale, protect the initial investment, or avoid wasting what has already been spent.

Sometimes the request is correct. Often it reflects escalation.

Governance test: A second tranche should be approved only after a fresh review of evidence, assumptions, operating burden, and alternatives. Prior spend should explain context; it should not determine continuation.

5. A Better Capital Budgeting Doctrine

A serious capital process treats every major proposal as five claims.

1. The Economic Claim

The proposal should identify:

| Element | Required Disclosure |

|---|---|

| cash-flow source | revenue, cost reduction, risk reduction, option value |

| unit economics | price, cost, margin, volume |

| scale channel | how cash flow grows |

| capital at risk | committed, staged, and irreversible capital |

| sensitivity drivers | variables that move the case |

| cash timing | when cash leaves and returns |

| downside economics | plausible adverse case |

2. The Strategic Claim

The proposal should identify the strategic asset being built:

| Strategic Asset | Example |

|---|---|

| capability | manufacturing, data, distribution, technical competence |

| position | market access, channel control, customer lock-in |

| option | future product, geography, platform, regulatory pathway |

| resilience | supplier redundancy, security, continuity |

| control | IP, infrastructure, data, standards, talent |

A strategic claim deserves respect when the asset is named, measured, and governed.

3. The Operating Claim

The proposal should identify:

- implementation owner;

- affected functions;

- handoffs;

- talent load;

- systems burden;

- customer disruption;

- support cost;

- quality controls;

- governance load.

The functions carrying the work should sign the burden estimate.

4. The Political Incidence Claim

Political incidence means the internal distribution of benefit, burden, status, and control.

The proposal should identify:

| Question | Purpose |

|---|---|

| Who sponsors the project? | accountability |

| Which unit benefits? | internal upside |

| Which unit carries the work? | operating burden |

| Which unit loses resources or autonomy? | tradeoff visibility |

| Which executive narrative is strengthened? | institutional meaning |

| Which alternatives lacked sponsorship? | fairness and completeness |

| Which veto points remain? | execution realism |

This is an incidence analysis, not a character judgment.

5. The Abandonment Claim

The proposal should identify:

- early evidence threshold;

- stage-gate timing;

- stop condition;

- second-tranche condition;

- owner of the stop decision;

- board escalation trigger.

A project without an abandonment rule has already begun to behave like a political commitment.

6. Capital Budgeting Audit

Before approval, use this audit.

| Question | Required Evidence |

|---|---|

| What problem does this investment solve? | One-sentence problem statement and current cost of the problem |

| Why this project now? | Timing rationale and rejected alternatives |

| What cash flow does the project produce? | Revenue, margin, cost-reduction, or risk-reduction mechanism |

| Which assumptions drive the model? | Top five sensitivities ranked by cash and strategic impact |

| Who carries the implementation burden? | Named functional owners and capacity estimates |

| Which costs sit outside the model? | Integration, training, support, quality, governance, switching costs |

| Which internal interests benefit from approval? | Sponsor, division, capability, status, budget, strategic narrative |

| Who loses resources, autonomy, or attention? | Affected functions and tradeoffs |

| What evidence would require withdrawal? | Stage-gate, threshold, and abandonment rule |

| Who is accountable after approval? | Sponsor and operating owner tied to post-approval metrics |

The audit converts the proposal from persuasion into decision.

7. Board and C-Suite Questions

Executives should ask:

- Which assumption, if wrong, damages the case most severely?

- Which function carries the largest burden outside the model?

- Which executive or division benefits most from approval?

- Which alternative was rejected on evidence, and which alternative lacked sponsorship?

- Is the discount rate doing economic work or political work?

- Does “strategic” identify an asset, a capability, or an unmeasured preference?

- What happens after the first tranche disappoints?

- Which leading indicator will warn us early?

- Who has authority to stop the project?

- Would the same proposal receive the same capital if brought by a weaker sponsor?

The last question is the cleanest test of institutional discipline.

8. The Stage-Gate Rule

Large projects should receive commitment in tranches.

Each tranche should carry:

- a defined objective;

- a measurement packet;

- an operating owner;

- a finance owner;

- an evidence threshold;

- a stop condition;

- a board escalation rule.

| Stage | Capital Release | Evidence Required |

|---|---|---|

| Concept | Small | problem evidence, strategic fit, option value |

| Pilot | Limited | technical feasibility, customer validation, operating burden |

| Scale readiness | Moderate | repeatability, unit economics, channel capacity, support model |

| Full scale | Large | leading indicators, absorption capacity, governance readiness |

Stage-gating preserves learning while limiting political momentum.

9. Sponsorship Has a Proper Role

Major investment needs sponsorship. An organization rarely builds a new future without internal advocacy.

Healthy sponsorship does three things:

- It brings the proposal into the institution.

- It assembles the coalition required for execution.

- It accepts evidence-based discipline after approval.

Unhealthy sponsorship substitutes status for evidence. It treats cancellation as humiliation and variance as a communications problem.

The distinction:

| Healthy Sponsorship | Unhealthy Sponsorship |

|---|---|

| names the uncertainty | hides the uncertainty |

| accepts stage-gates | seeks full commitment early |

| protects disciplined learning | protects reputation |

| clarifies operating burden | exports burden to others |

| welcomes challenge | treats challenge as disloyalty |

| preserves abandonment authority | escalates after weak evidence |

A mature capital process does not purge politics. It makes internal influence visible and answerable to evidence.

Closing

Capital budgeting is one of the principal ways strategy becomes real. It decides which future receives cash, talent, attention, legitimacy, and patience.

The spreadsheet is indispensable. The process around the spreadsheet is decisive.

A serious enterprise reads every capital model twice: once as finance and once as institutional incidence. The first reading asks whether the economics work. The second asks whose priorities, burdens, and authority the model advances.

The rule is simple:

Approve capital only when the economics, operating burden, political incidence, and abandonment rule are visible together.

Sources

- Joseph L. Bower, Managing the Resource Allocation Process: A Study of Corporate Planning and Investment, Harvard Business School, 1970. Bower’s work is foundational for treating resource allocation as an organizational process rather than a pure financial calculation.

- Richard M. Cyert and James G. March, A Behavioral Theory of the Firm, 1963. The behavioral theory of the firm treats organizations as coalitions with bounded rationality, negotiated goals, and satisficing behavior.

- Michael D. Cohen, James G. March, and Johan P. Olsen, “A Garbage Can Model of Organizational Choice,” Administrative Science Quarterly 17, no. 1 (1972): 1–25. The model describes decision-making under problematic preferences, unclear technology, and fluid participation.

- Kathleen M. Eisenhardt and Mark J. Zbaracki, “Strategic Decision Making,” Strategic Management Journal 13 (1992): 17–32. The article is a major review of rationality, bounded rationality, and politics in strategic decision-making.

- Barry M. Staw, “Knee-deep in the Big Muddy: A Study of Escalating Commitment to a Chosen Course of Action,” Organizational Behavior and Human Performance 16, no. 1 (1976): 27–44. The paper is the classic starting point for escalation-of-commitment research.

- Steven Kerr, “On the Folly of Rewarding A, While Hoping for B,” Academy of Management Journal 18, no. 4 (1975): 769–783. Kerr’s incentive critique is directly relevant to budget approval processes that reward project capture rather than value realization.